Stainless Steel MMI: Nickel Prices Move Sideways, Begin to Climb in September

By Nichole Bastin and Katie Benchina Olsen

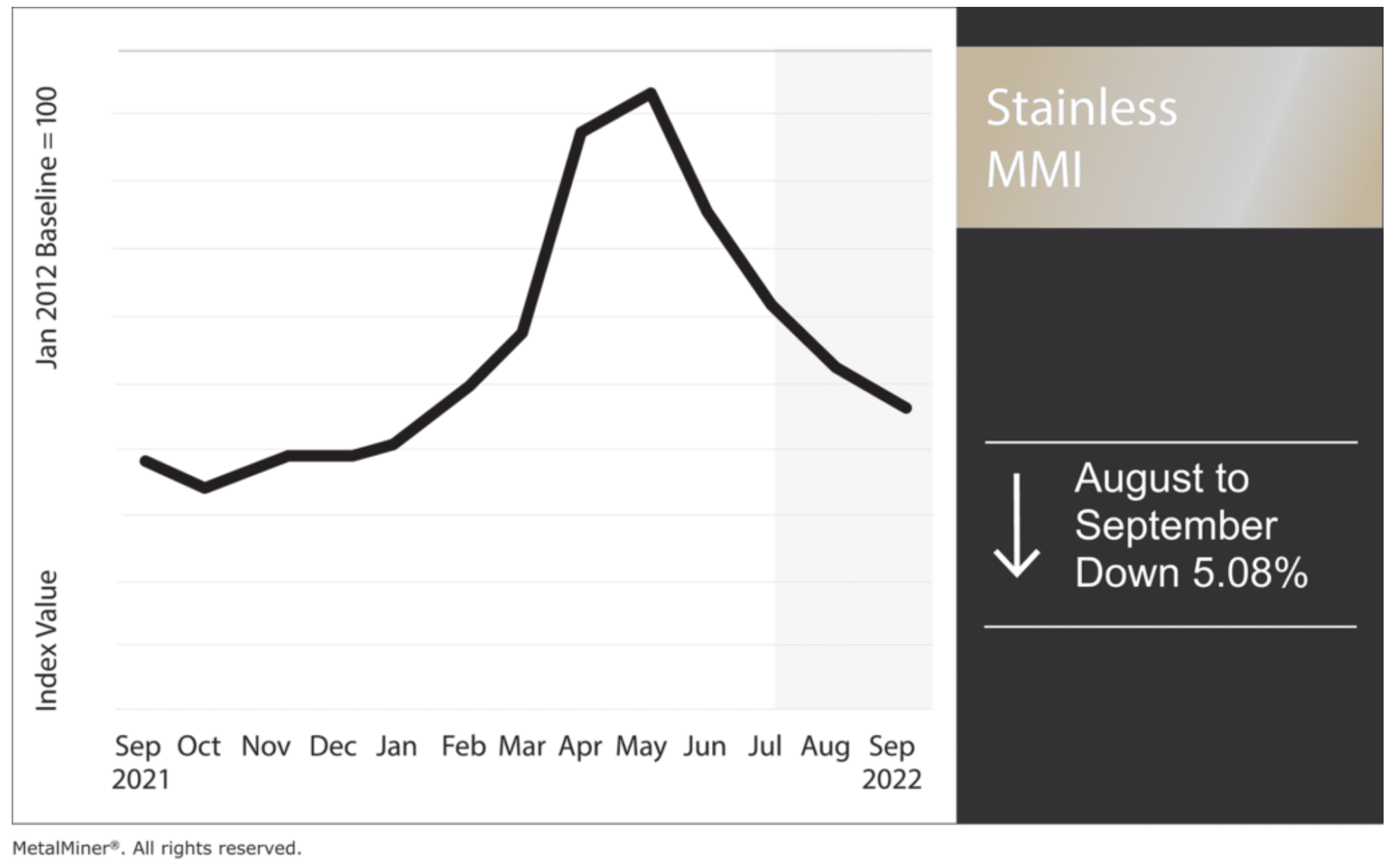

The Stainless Steel Monthly Metals Index (MMI) dropped 5.08% from August to September.

Nickel prices began to rise this month, breaking through prior highs visible on shorter time frames such as the hourly and daily charts. Ultimately, prices bounced off bullish zones formed before the LME’s shutdown in March. This price action indicates nickel has the potential for upside reversal if prices continue to push up. Overall, however, prices remain in a mid-to-long-timeframe trading range. Investors will need to break this to establish a new long-term trend.

Learn how to gauge metal prices in MetalMiner’s free September Webinar. Sign up here!

High Inventory Levels Among Service Centers, Manufacturers, and End Users

Stainless flat-rolled inventories have not only built up at service centers but also at some manufacturers and end-user locations. In fact, sources tell MetalMiner that service center inventories are averaging between three and four months of supply. Optimally, service centers would only have around two months of supply. MetalMiner has also received word that some end users have more than nine months of inventory on their floors. Obviously, if end users and manufacturers are this flush with inventory, it impacts service center shipments.

The big question: how did this happen?

Entering 2022, U.S. flat-rolled stainless steel production remained constrained by strict allocations of alloys, widths, and thicknesses as directed by production mills. So, to maximize production output, North American Stainless and Outokumpu focused on producing standard 304 / 304L along with some 316L. These were mostly in widths 48″ and greater and thicknesses heavier than 0.035”. Width, light gauge and alloy extras came about to penalize products that drained output capacity. On top of that, some stainless buyers also hedged their bets by over-forecasting 2022 requirements with the expectation that supply disruptions would continue.

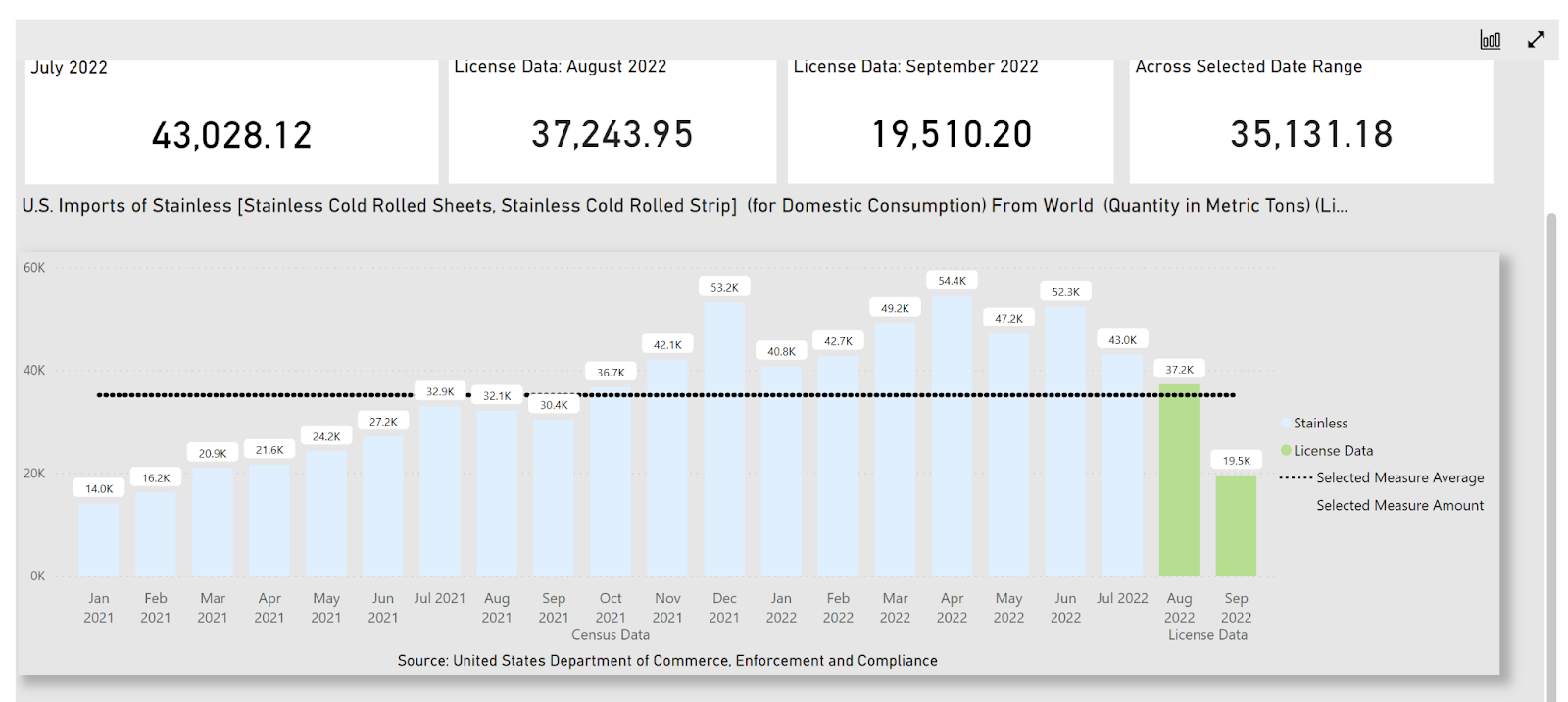

Meanwhile, stainless cold rolled imports rose continuously throughout 2022, peaking between April and June. This helped bridge the U.S. supply gap, and imports started to wane as service center inventories became more robust. And despite aggressively-priced import offers, service centers soon began to pull back. Imports don’t necessarily arrive in the same month they’re ordered. Because of this, cold rolled imports continue to show up (though in much lower volumes).

SIMA Stainless cold rolled sheet and strip imports into the US.

Stainless Steel Inventory Issues Should Resolve Soon

Many of the manufacturers who overbought to avoid outages now have too much inventory. All of their sources have delivered the agreed-upon quantities, and the companies have no choice but to wait. Fortunately, those businesses that buy excess from end users may be able to reduce the latter’s inventory exposure and free up some cash. Currently, service centers are not going to buy back excess inventories. However, there are some B2B companies that specialize in aligning sellers with buyers in this situation.

Several of MetalMiner’s sources suggest that the problem of increased service center inventories may resolve as early as the end of 2022 and as late as Q1 2023. However, it’s important to also consider the potential devaluation of these inventories as 2022 marches on. For example, the 304 alloy surcharge continues to decline from its May peak. September’s 304 surcharge is also $1.2266 / lb, which is $0.6765 / lb lower than those seen in May.

Check out MetalMiner’s stainless steel should cost models by scheduling a demo of the Insights platform.

U.S. and EU Nickel Imports From Russia Surge

Untouched by sanctions, Western nations continue to import Russian nickel. Indeed, shipments have actually increased since March. Russia accounts for roughly 7% of global nickel production, and its largest company, Nornickel, produces roughly 15-20% of global battery-grade nickel.

The U.S. saw the largest increase. According to data from the United Nations Comtrade database compiled by Reuters, nickel imports from Russia to the U.S. jumped 70% from March through June. Meanwhile, imports to the EU during that same time rose 22%.

The increase in Russian-sourced material indicates two things. First, lower prices have likely increased the appeal of Russian nickel, as all other prices rose following the Ukraine invasion. Second, it means that the concerns over supply disruptions that caused base metal prices to surge in early March have proven overstated.

Stay up to date on MetalMiner and the stainless steel industry with weekly updates – without the sales pitch. Sign up for MetalMiner’s weekly newsletter.

But the Buying Frenzy May Not Last

As the 2023 contract season begins, Western manufacturers may start to wean themselves off Russian supply.

According to Paul Warton, Executive Vice President for Norsk Hydro’s extruded aluminum products business, “we categorically will not be buying from Russia for 2023.” Novelis Inc. has also begun to shun Russian material as it looks to feed its factories next year. In fact, early negotiations with Nornickel indicate that European buyers want to reduce their purchases almost across the board.

These sourcing shifts will likely serve to divert discounted material to companies and countries still willing to import from Russia. “I don’t know where that material will flow to now – maybe into Asia, China, Turkey, and other areas that haven’t taken as tough a stance on Russian material,” Warton added.

This could cause material sourced elsewhere to carry a larger premium. Of course, not all companies will adopt this hard-lined approach toward Russian material. And because such abstinence is self-imposed, it won’t eliminate Russian nickel from the global market.

The MetalMiner Annual Outlook for 2023 comes out this week! The report consolidates our 12-month view and provides buying organizations with a complete understanding of the fundamental factors driving prices and a detailed forecast that can be used when sourcing metals for 2023 — including expected average prices, support and resistance levels.

Biggest Nickel and Stainless Steel Price Moves

- Chinese ferromolybdenum lumps rose by 7.96% to $25,531 per metric ton as of September 1.

- Indian primary nickel prices rose 2.95% to $24.32 per kilogram.

- Meanwhile, Korean 430 cold rolled coil dropped 9.24% to 1,596 per metric ton.

- Korean 304 cold rolled coil fell 10.15% to 2,938 per metric ton.

- Chinese primary nickel declined 12.56% to 24,937 per metric ton.

Leave a Reply