Download our mobile app to

your devices

China Weekly Inventory Summary and Data Wrap (Nov 4)

Source:SMM

This is a roundup of China's metals weekly inventory as of November 4.

SHANGHAI, Nov 4 (SMM) - This is a roundup of China's metals weekly inventory as of November 4.

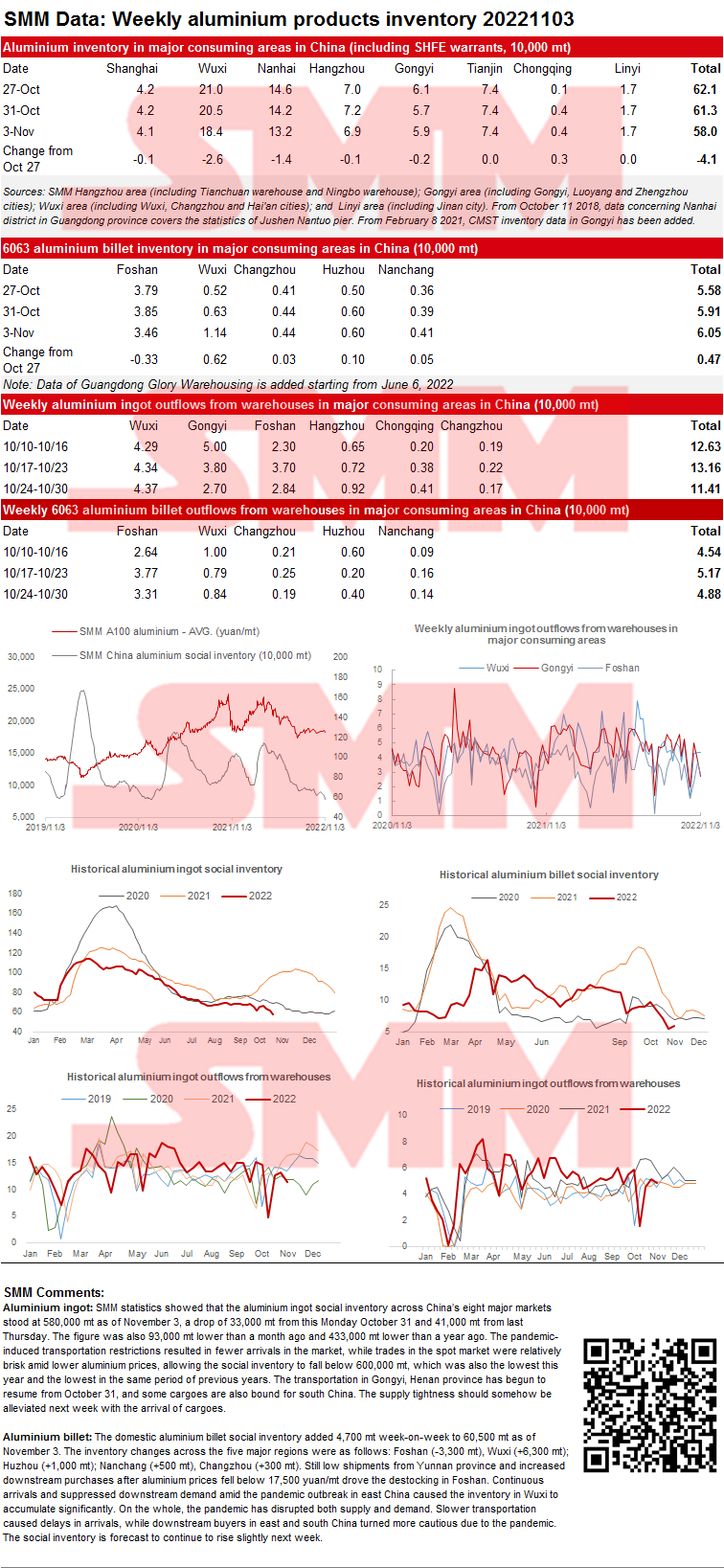

SMM Updates on China Aluminium Ingot and Billet Social Inventories as of November 3

Aluminium ingot: SMM statistics showed that the aluminium ingot social inventory across China’s eight major markets stood at 580,000 mt as of November 3, a drop of 33,000 mt from this Monday October 31 and 41,000 mt from last Thursday. The figure was also 93,000 mt lower than a month ago and 433,000 mt lower than a year ago. The pandemic-induced transportation restrictions resulted in fewer arrivals in the market, while trades in the spot market were relatively brisk amid lower aluminium prices, allowing the social inventory to fall below 600,000 mt, which was also the lowest this year and the lowest in the same period of previous years. The transportation in Gongyi, Henan province has begun to resume from October 31, and some cargoes are also bound for south China. The supply tightness should somehow be alleviated next week with the arrival of cargoes.

Aluminium billet: The domestic aluminium billet social inventory added 4,700 mt week-on-week to 60,500 mt as of November 3. The inventory changes across the five major regions were as follows: Foshan (-3,300 mt), Wuxi (+6,300 mt); Huzhou (+1,000 mt); Nanchang (+500 mt), Changzhou (+300 mt). Still low shipments from Yunnan province and increased downstream purchases after aluminium prices fell below 17,500 yuan/mt drove the destocking in Foshan. Continuous arrivals and suppressed downstream demand amid the pandemic outbreak in east China caused the inventory in Wuxi to accumulate significantly. On the whole, the pandemic has disrupted both supply and demand. Slower transportation caused delays in arrivals, while downstream buyers in east and south China turned more cautious due to the pandemic. The social inventory is forecast to continue to rise slightly next week.

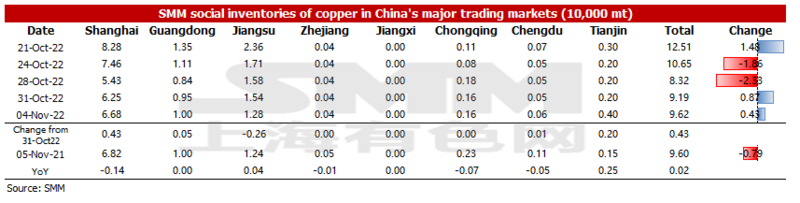

Copper Inventory across Major Chinese Markets Add 4,300 mt from Monday

As of Friday November 4, SMM copper inventory across major Chinese markets stood at 96,200 mt, up 4,300 mt from Monday and 13,000 mt from last Friday. Compared with the data on Monday, the inventory in all regions of China increased except that in Jiangsu. The total inventory was 200 mt higher than in the same period last year when the figure was 96,000 mt. Among them, the inventory in Shanghai dipped 1,400 mt YoY, that in Guangdong stood flat, that in Jiangsu added 400 mt, and that in Tianjin rose 2,500 mt. The supply increased while the demand weakened this week.

In detail, the inventory in Shanghai added 4,300 mt to 66,800 mt from Monday because imported copper that should arrive in Shanghai finally arrived this week. The inventory in Guangdong grew 500 mt to 10,000 mt owing to the continuous arrival of goods shipped from east China to factories, resulting in a decrease in shipments flowing out of the warehouses in Guangdong. In Tianjin, due to poor local consumption and the large spread between the copper cathode and copper scrap, the demand for copper cathode remained sluggish, thus the inventory rose 2,000 mt to 4,000 mt.

Looking ahead, the market will witness more imported copper arriving at ports next week, and the domestic supply may remain stable. In terms of consumption, the market shall keep an eye on whether copper prices can fall. If the spread between the copper cathode and copper scrap was not wide, the copper cathode consumption might not improve. Therefore, the inventory will grow slightly next week.

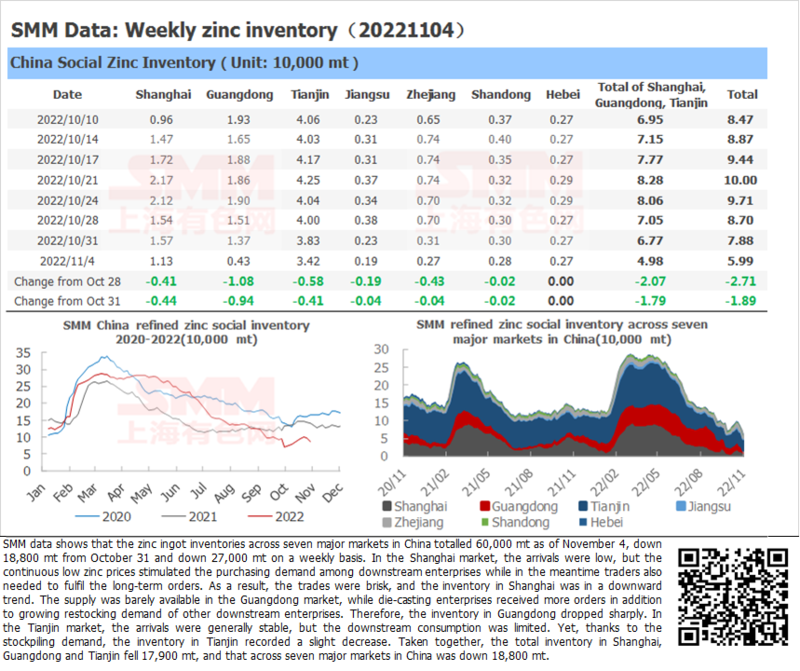

Zinc Ingot Social Inventory Down 18,800 mt from Monday

SMM data shows that the zinc ingot social inventories across seven major markets in China totalled 60,000 mt as of November 4, down 18,800 mt from October 31 and down 27,000 mt on a weekly basis. In the Shanghai market, the arrivals were low, but the continuous low zinc prices stimulated the purchasing demand among downstream enterprises while in the meantime traders also needed to fulfil the long-term orders. As a result, the trades were brisk, and the inventory in Shanghai was in a downward trend. The supply was barely available in the Guangdong market, while die-casting enterprises received more orders in addition to growing restocking demand of other downstream enterprises. Therefore, the inventory in Guangdong dropped sharply. In the Tianjin market, the arrivals were generally stable, but the downstream consumption was limited. Yet, thanks to the stockpiling demand, the inventory in Tianjin recorded a slight decrease. Taken together, the total inventory in Shanghai, Guangdong and Tianjin fell 17,900 mt, and that across seven major markets in China was down 18,800 mt.

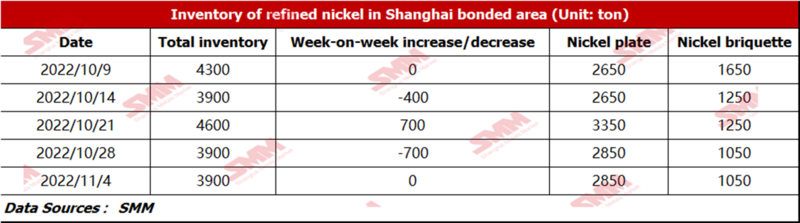

Bonded Zone Inventory of Nickel Stays Almost Unchanged on the Week

According to SMM research, the bonded zone inventory of nickel stood at 3,900 mt this week. The inventory of nickel briquette was 1,050 mt, and that of nickel plate stood at 2,850 mt. Almost no imported nickel products in the bonded zone warehouses cleared customs in the week amid the import losses of about 9,000 yuan/mt, the off-season of stainless steel, alloy and electroplating industries, and the slack downstream demand for nickel plate caused by the soaring SHFE nickel.

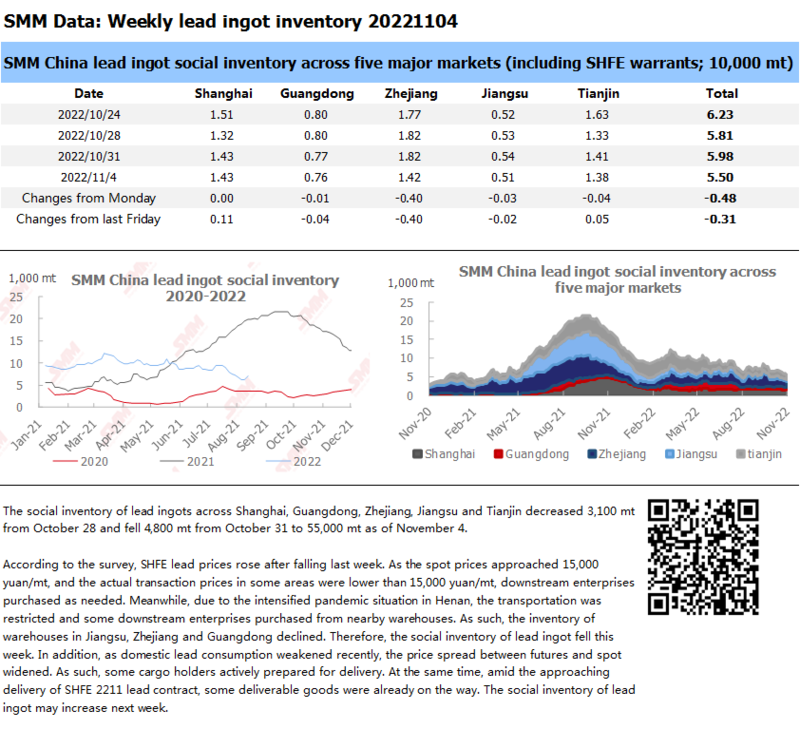

Social Inventory of Lead Ingot Declines amid Low Prices, Follow-Up Attention Should be Paid to the Delivery of SHFE 2211 Lead contract

The social inventory of lead ingots across Shanghai, Guangdong, Zhejiang, Jiangsu and Tianjin decreased 3,100 mt from October 28 and fell 4,800 mt from October 31 to 55,000 mt as of November 4.

According to the survey, SHFE lead prices rose after falling last week. As the spot prices approached 15,000 yuan/mt, and the actual transaction prices in some areas were lower than 15,000 yuan/mt, downstream enterprises purchased as needed. Meanwhile, due to the intensified pandemic situation in Henan, the transportation was restricted and some downstream enterprises purchased from nearby warehouses. As such, the inventory of warehouses in Jiangsu, Zhejiang and Guangdong declined. Therefore, the social inventory of lead ingot fell this week. In addition, as domestic lead consumption weakened recently, the price spread between futures and spot widened. As such, some cargo holders actively prepared for delivery. At the same time, amid the approaching delivery of SHFE 2211 lead contract, some deliverable goods were already on the way. The social inventory of lead ingot may increase next week.

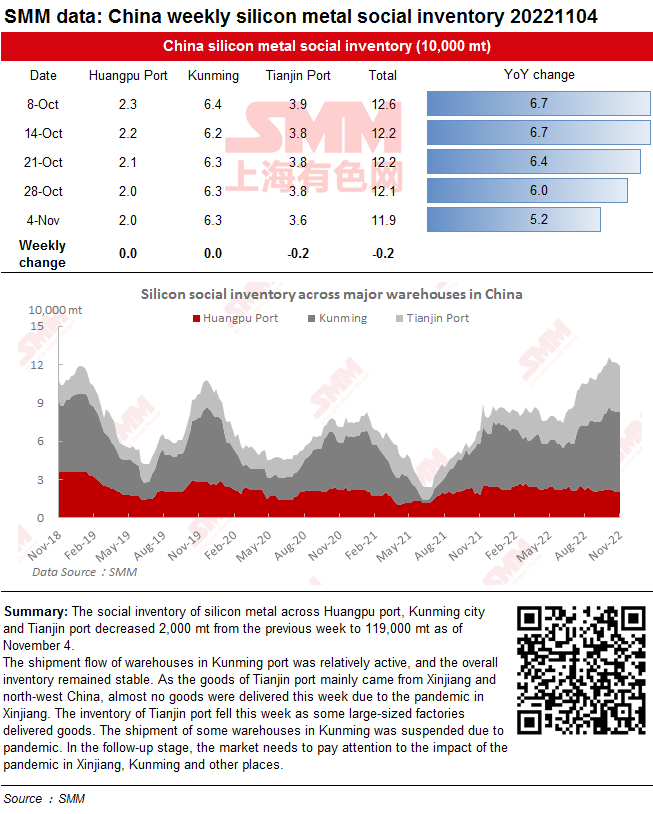

Social Inventory of Silicon Metal Declines amid the Pandemic

The social inventory of silicon metal across Huangpu port, Kunming city and Tianjin port decreased 2,000 mt from the previous week to 119,000 mt as of November 4.

The shipment flow of warehouses in Kunming port was relatively active, and the overall inventory remained stable. As the goods of Tianjin port mainly came from Xinjiang and north-west China, almost no goods were delivered this week due to the pandemic in Xinjiang. The inventory of Tianjin port fell this week as some large-sized factories delivered goods. The shipment of some warehouses in Kunming was suspended due to pandemic. In the follow-up stage, the market needs to pay attention to the impact of the pandemic in Xinjiang, Kunming and other places.

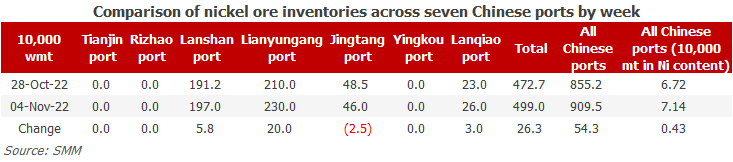

Nickel Ore Inventories at Chinese Ports Up 543,000 wmt WoW

As of November 4, the inventory of nickel ore across Chinese ports increased by 543,000 wmt to 9.095 million wmt compared with last Friday. The total Ni content stood at 71,000 mt. The total inventory at seven major ports across China stood at 4.99 million wmt, 263,000 wmt higher than last week. The rainy season began in the main mining areas in the Philippines in October, but the nickel ore stockpiled by NPI plants before the rainy season gradually arrived at ports, thus the port inventory increased. At the same time, the output growth of domestic NPI plants was limited in October and their in-plant inventories of nickel ore grew, slowing down the destocking of port inventory. The short-term port inventory of nickel ore will burgeon slightly.

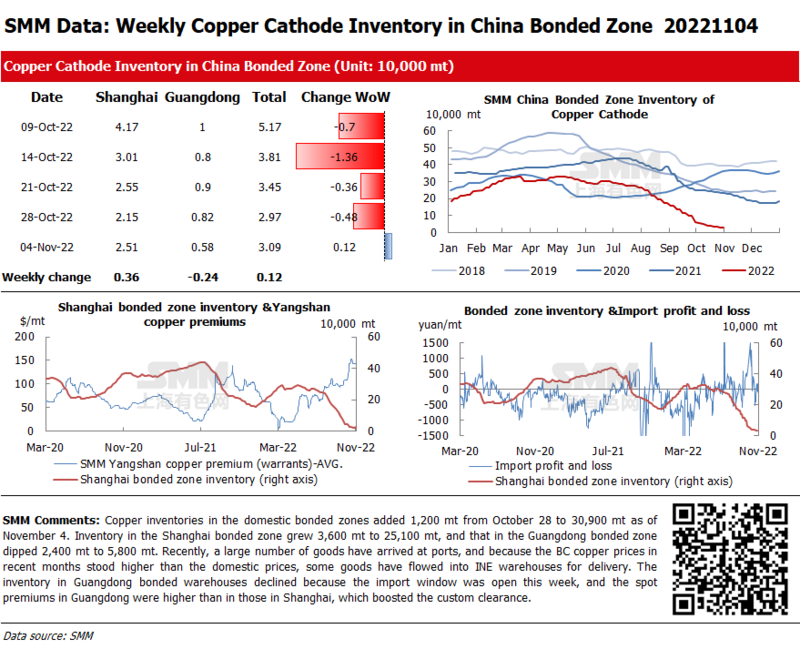

Copper Inventories in Domestic Bonded Zones Up 1,200 mt from October 28

Copper inventories in the domestic bonded zones added 1,200 mt from October 28 to 30,900 mt as of November 4. Inventory in the Shanghai bonded zone grew 3,600 mt to 25,100 mt, and that in the Guangdong bonded zone dipped 2,400 mt to 5,800 mt. Recently, a large number of goods have arrived at ports, and because the BC copper prices in recent months stood higher than the domestic prices, some goods have flowed into INE warehouses for delivery. The inventory in Guangdong bonded warehouses declined because the import window was open this week, and the spot premiums in Guangdong were higher than in those in Shanghai, which boosted the custom clearance.

Inventory

For queries, please contact Michael Jiang at michaeljiang@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn

Related news

SMM Events & Webinars

All- Oct08

2nd Li-ion Battery Europe 2024

Oct 08 - 10,2024THE EGG BRUSSELS, BELGIUM

- Jun24

2024 Global Renewable Metal Industry Chain Summit

Jun 24 - 25,2024To foster international cooperation and dialogue among industry colleaguesKuala Lumpur , Malaysia

- Jun18

2024 ASEAN Automotive Supply Chain

Jun 18 - 19,2024Pattaya,Thailand

Shanghai Metals Market

Privacy PolicyCompliance CentreSMM Credit ServiceContact UsAbout UsTerms & ConditionsSitemapHoliday Pricing Schedule

Notice: By accessing this site you agree that you will not copy or reproduce any part of its contents (including, but not limited to, single prices, graphs or news content) in any form or for any purpose whatsoever without the prior written consent of the publisher.

Drop us a line

service.en@smm.cn

How can we help you?

+86 021 5155-0306

Live chat via WhatsApp

Copyright © 2024 SMM Information & Technology Co., Ltd. All rights reserved.